The Future Cash Flow Strategy You Probably Didn’t Know Existed

Between rental, earned, profit, royalty, dividend, capital gains, and interest income, there are a plethora of passive income (i.e. requiring minimal effort on your part) strategies that you can engage in to ensure you are always getting the most out of your capital. Let’s briefly go through the highlights of seven streams of income before diving into an EIGHTH stream of income which we like to refer to as the “secret” income stream.

1. Rental Income

- Usually rises with inflation, thereby allowing you to ensure your capital does not succumb to the negative impacts of inflation.

2. Earned Income

- Wealth you accumulate through your professional career and provides a dependable and consistent income inflow.

3. Business Profits

- Money earned by a business that is left over after expenses are paid. While running your own business can provide some freedom, it doesn’t come without risk and depends on the stability of your industry.

4. Royalty Income

- A form of inactive income produced through creating or designing something new and unique, and charging a fee for individuals and organizations to utilize it.

- Assuming stable demand, it can enable you to be compensated inactively for your previous work and efforts for the rest of your life, with, in many cases no limits to the amount of capital you can accumulate.

5. Dividend Income

- Money you receive (generally monthly or quarterly—depending on the stock) simply for holding dividend-paying shares in your portfolio.

- Dividend income is inactive in nature rather than active—this income stream is automatic as the funds are deposited into your investment account (however, it’s important to note that some stocks do change or cut dividends from time to time, and income is never 100% guaranteed). Once you or your investment manager have performed research on which stocks are right for you, assuming you are engaging in a long-term position, there is no further action you need to take!

6. Interest Income

- The amount earned for lending money or letting another entity use your funds with very limited work required on your part, however, while interest on an account can be compounded, interest rates may be lower than the yield from other income streams.

7. Capital Gains Income

- Taxed at favorable rates in Canada—meaning you get to keep more in your pocket. Capital gains income is earned when you sell an asset for more than you paid for it.

Now that we have briefly recapped the seven streams of income, if we were to tell you there is another asset class that can provide an eighth stream of passive income would you be interested?

What are the Characteristics of This Investment (Future Cash Flow Strategy)?

- Like a market rate GIC, any capital invested is guaranteed, yet can benefit from upside market performance.

- Growth in value over time is sheltered from taxation as long as the growth is retained inside the asset.

- Its structure does not allow it to have any negative growth.

- The transfer of this asset after death is tax-free and not subject to any probate or estate administration fees.

- It invests in conservative instruments with very low volatility and therefore can be more predictable than many other options.

- Its value, at the death of the owner, is not subject to market conditions at the time, unlike real estate

- When transferred at death, complete confidentiality is maintained as it is not required to be included in any will.

Just as significantly, this asset can provide additional cash flow on a level, periodic or even ad hoc basis.

Now, here’s the thing—this all can happen within a well-designed insurance contract. Wait! We understand that many people run away when they hear the word insurance. The reason we look at using this strategy is not because you need insurance (most people have that need taken care of)—it is because of the tax minimization and deferral benefits, which are not found in other passive income strategies.

Furthermore, insurance provides intangible benefits through serving as a diversification tool and as a way to provide confidence to family members in the event of an untimely passing.

Why Do Permanent Policies have such Poor Reputations?

Permanent insurance has had its reputation tainted over the last number of years. When presenting whole life or universal life policies to clients, the assumptions that were used for policy performance were overstated, creating unreasonable expectations of future values.

After 2008, investment returns (whether selected by the policyowner in a universal life policy or the insurance company with a whole life policy, along with interest rates) have been significantly lower than in the decade prior to that.

Since interest rates, which impact the performance of many other investment vehicles are historically low, the time has never been better to consider a whole life policy, as long term projections point to increased rates and policy performance over time.

Illustrations today reflect growth projections that, while not guaranteed, are much more conservative and more achievable than in years past. As stated above, however, capital invested is always guaranteed.

Whom is This Strategy Ideal for?

Another reason that permanent insurance has a poor reputation is because oftentimes, it’s sold despite not always being an appropriate solution.

When sold appropriately, permanent insurance is an investment and diversification opportunity. It’s available and really only appropriate for clients who have large amounts of surplus cash flow and are seeking diversification strategies.

Typically, these clients have maximized other vehicles like their RRSP and TFSA. Clients who are considering this type of strategy should be prepared for a commitment of at least 10 years of deposits. This affords the policy time to accumulate more significant cash value which will ultimately be the driver of the cash flow available.

An individual or corporate entity can purchase as many policies as they like, with no limit on the amounts that can be deposited, provided they can qualify both medically, and financially which is determined by the insurance carrier. In all cases, the death benefit proceeds are received by the beneficiaries, whether an individual, a corporation, or other entity, on a tax-free basis. These proceeds are not included in any probate or estate administration assessments.

Let’s briefly look at what is currently available in the marketplace today, why this strategy should be explored, and which type of insurance may be appropriate for your current situation.

What are the Three Types of Life Insurance and What are the Pros and Cons?

- Term Insurance:

- This type of insurance provides death benefit coverage only. It is issued for fixed periods of time, such as 10 years or 20 years.

- During that period the cost is guaranteed, level, and initially much lower than other kinds of insurance. When the period is up, most of these types of policies will renew at a significantly higher premium for another period of the same duration.

- These policies usually terminate at a given age, so they are not recommended for any long term or estate planning purposes. Term policies are most often recommended to offset the liability of a term debt, such as a mortgage. They are designed to address a limited term need–once the mortgage has been paid off, that need no longer exists.

- Younger families where income levels might be limited but family obligations may require large amounts of coverage are also prime candidates for term insurance, with its relatively low cost.

- Universal Life Insurance:

- This type of insurance provides the policyowner with more flexibility in terms of product configuration.

- For the initial face amount of coverage, the policyowner can establish a deposit pattern that might be more aligned to his or her income stream, as long as the minimum deposit necessary to support the coverage amount is provided.

- The structure permits deposits over and above this minimum amount, within limits, which are then invested in a range of options chosen by the policyowner.

- Any growth in the investment account is sheltered from any taxation as long as it is not withdrawn from the policy.

- The death benefit type is also controlled by the policyowner, who may elect to have the total death benefit be the sum of the face amount plus the investment account.

- The risk here is that the investment account balance, and therefore the total payout can vary along with account balance. Gains over several years could be reversed with a potential drop in the investment option performance.

- As long as adequate deposits to the policy are being made, or there is sufficient value in the investment account portion of the policy to pay any insurance costs, the policy will stay in effect.

- Whole Life or Participating Life Insurance:

- This is another type of permanent life insurance but unlike Universal Life policies, the cost of insurance charges and investment component of any deposits are ‘blended’.

- It is the insurance company that determines the investment options, and the returns from the investments are credited to the policy in the form of a dividend.

- Owners of these policies can select the manner in which the dividends are treated. They can be paid out each year in cash; they can be applied to the premium required; they can purchase additional term insurance coverage; but in most cases they will purchase additional layers of permanent insurance coverage, growing the ultimate death benefit payout.

- Besides the dividend, these policies have a guaranteed cash value, regardless of any investment performance. As such, these policies are guaranteed to grow in value each year, although the rate of growth is variable.

- Many who look at this strategy have already maximized their RRSP and TFSA contributions. Both of these can provide significant benefits, but are also subject to a number of government rules and deposit levels which is why whole life policies could be an appropriate diversification strategy for some.

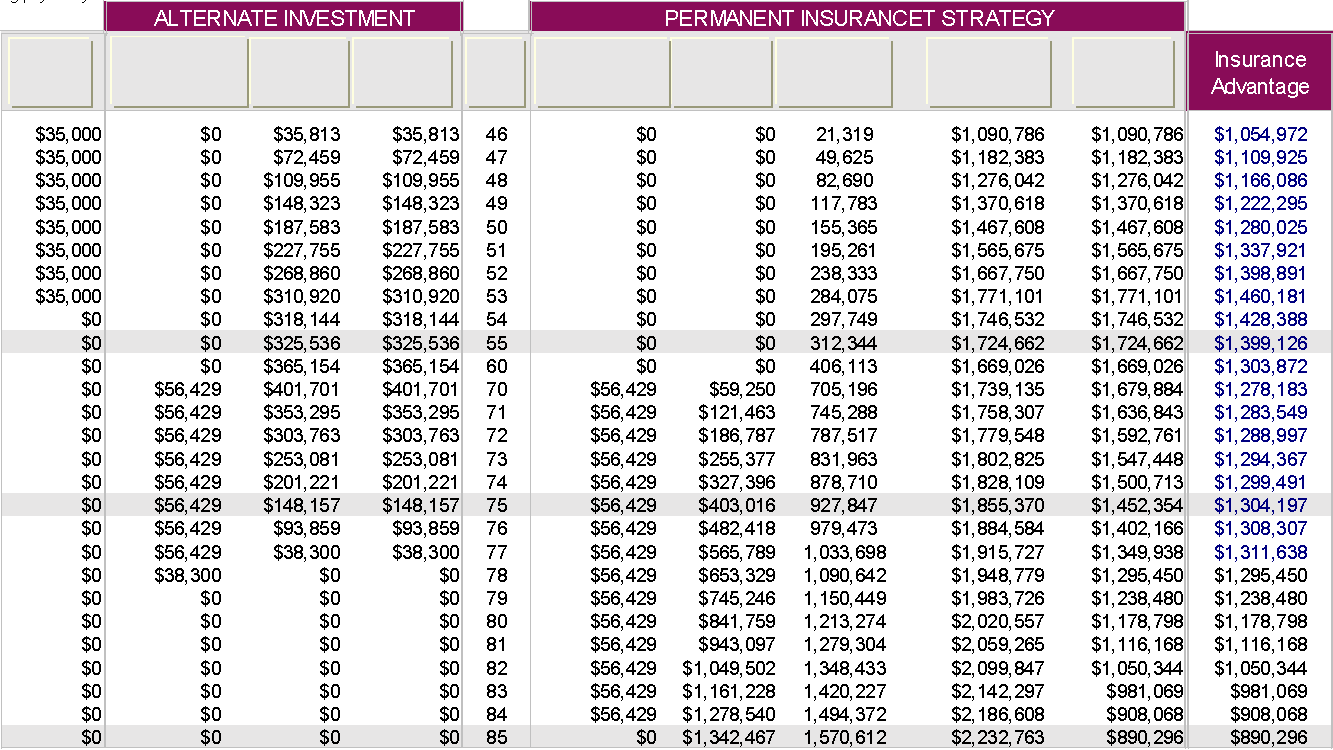

What is an Example of a Life Insurance Strategy?

Here is a real world example of how a properly structured, whole life contract could work for you.

Jack and Jill are already maxing their RRSP and TFSA contributions, but still have surplus cash flow of $35,000 annually they wish to set aside to provide some additional cash flow during their retirement years. Their advisor shows them a comparison of depositing the surplus into a non-registered plan or a permanent insurance policy. The deposits are made for 8 years, and then left to accumulate in both options. While initially income is drawn from the registered plans, by age 70, Jack and Jill wish to draw the additional cash flow they will need. When comparing the two investment options, the insurance strategy can provide $56,000 per year, tax-free, for 15 years. The alternate investment can match the $56,000, but would be fully depleted in under 9 years. In addition, although the traditional investment has no benefit left for Jack and Jill’s estate, the insurance policy still has an additional $890,000 at life expectancy (Manulife Par Joint last to Die).

Insurance Income section written with the help of David Rubin, Estate & Insurance Advisor.

Preserve and Build Your Wealth with Bloom

At Bloom Investment Counsel, Inc., our goal is to help ensure your money is working for you, and not the other way around. Bloom is pleased to assist wealthy individuals, foundations, corporations, institutions and trusts in achieving financial independence by drawing upon a myriad of income strategies—skillfully capitalizing on the wealth of returns produced in the form of dividends, capital gains, and interest income.

Our methodology has worked for countless clients—we proudly have over 36 years of experience under our belts, and have managed over $2.5 billion in assets. Further to this, Bloom can work with your advisors and partners to help you obtain other four possible income streams—because at Bloom, we believe you should never put all of your eggs in one basket. Let’s talk to learn more about the ways in which you can experience financial freedom with multiple, steady, and reliable income streams.

This content is provided for general informational purposes only and does not constitute financial, investment, tax, legal or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this content should consult with his or her financial partner or advisor.