The Ultimate Guide To Maximize Your Giving

While many of us feel an intrinsic pull to want to help those in need, when it comes to the tax and insurance implications involved when giving to charitable organizations, things can start to feel overly complicated quite quickly.

Not to worry—this guide is here to break things down in an easy-to-follow format, so that you can get back to supporting your community while having the peace of mind that you’re engaging in all of the best practices to make the most of your efforts from a financial perspective!

It Pays To Incite Meaningful Change!

In this guide, Bloom Investment Counsel, Inc. takes you through some of the top strategies for ensuring your giving is as financially effective as possible. We’ll be touching on everything from the purposes of charitable giving to an in-depth, simple to understand analysis of how life insurance maximizes your donations.

We’ll also shed some light on some recent Canadian tax and charity statistics.

Are you looking to capitalize on taxable benefits while giving back to your community? Settle in with Bloom Investment Counsel’s Maximize Your Giving – The Ultimate Guide to be on your way to implementing all of the best approaches!

This guide is brought to you in collaboration with David Rubin, Estate & Insurance Advisor.

What Are The Purposes Of Charitable Giving?

When you opt to give to a philanthropic effort, you are not only helping the organization at hand and those it helps, but you’re also obtaining many personal advantages—both intrinsic and financial. Some benefits include:

1. Tax Benefits

Perhaps the most common benefit one associates with donating to charitable causes is the tax advantages. These can vary from province to province, so Red Cross’ Donor Tax Credit Calculator is a great resource to reference if you’re looking to explore the tax credits arising from your generosity.

2. Boost Your Mood

There’s no question that helping others in need causes us to feel a sense of purpose, and increases feelings of happiness. When you donate to a cause you’re passionate about, you not only allow a charity to further their imperative work, but you’re also contributing to your emotional and mental wellness—which benefits all parties involved!

3. Fortify Your Personal Values

According to a study by Charities Aids Foundations, a feeling of integrity was the most widely reported response for why we give to philanthropic endeavours. An overwhelming 96% of participants stated they felt they had an ethical responsibility to use their own resources to aid others—a feeling deeply embedded in personal principles.

Leveraging Life Insurance to Maximize Your Charitable Giving Objectives

If you have a charitable organization you’re passionate about, you may consider donating your life insurance policy or policies, as a method for leaving a lasting legacy and to continue to aid a cause you care about deeply.

Your Policy, Your Terms

Gifting a life insurance policy to a registered charity is not subject to taxes. You’re able to structure your gift so that it fits your preferences and goals—to make a significant impact, you might consider setting up monthly or yearly payments in the amount of your choice. While you’re making a lasting impression and helping those in need, you also reap the benefits of the charitable tax receipts you obtain in exchange for your contribution.

3 Simple Methods For Donating Your Life Insurance Policy

1. Obtain A New Policy Naming The Registered Charity/Charities As The Owner

You will collect charitable tax receipts for the value of the policy for any premiums you pay.

2. Transfer Ownership Of A Current Policy To The Charity

Obtain a charitable tax receipt for the cash value of the policy. You may still need to pay any annual premiums owing, should there be any, but you will be able to collect additional tax receipts in the amounts of your payments.

3. Name The Charity As The Beneficiary Of A Pre-Existing Policy

If you already possess one or more life insurance policies, or your family already has financial security, this may be a good option for you. At the time of passing, the organization of your choosing will receive the policy proceeds and you will receive a tax receipt which can be applied to your terminal tax return. By naming the charity directly, the proceeds are not included in any probate or estate administration tax calculation.

Charity Tax In Canada: Some Recent Statistics

- Nationwide, the median donation claimed by tax filers in 2019 was $310.

- The province/territory that reported the highest median donation in 2019 was Nunavut at $630. While the territory saw the highest median donation total, it also had the lowest percentage of tax donors that filed of all provinces and territories, at just 6.2%.

- According to a recent StatsCan study, Canadians with incomes in excess of $80,000 are more likely to make charitable contributions, versus individuals in lower income brackets. This is unsurprising, as those with higher incomes have more disposable income from which to make donations.

- Claiming tax benefits is less common amongst young Canadian adults—the concept of utilizing donations as a means to reduce income tax is likely not yet a central concern. Furthermore, the lack of disposable income that is prevalent amongst younger age groups is also likely a contributing factor for why Canadian young adults do not see high donation rates.

Maximizing Tax Benefits With Your Charitable Giving: Some Real-World Examples

The following real world examples provide some insights into how you can ensure you’re maximizing your tax benefits whilst giving to philanthropic endeavours.

Example 1

John Smith was retiring after a long and successful career building up an incredibly profitable company. After selling his interest in the business, John and his wife Mary, although having always donated to worthy causes throughout the years, were looking to create a foundation, whereby they could continue their philanthropic efforts during their retirement years.

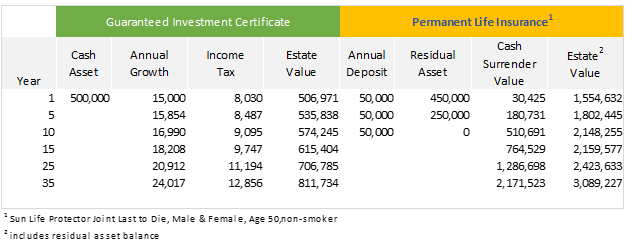

After consulting with their tax advisors, John and Mary decided to donate $1,000,000 to the private foundation they had set up. This provided a tax refund of $500,000, which they then used to make annual deposits of $50,000 for 10 years into a permanent insurance contract. The foundation was able to direct donations to a number of causes that John and Mary could select each year, while the policy would provide an even larger inheritance to their children than they would have otherwise received.

The table below shows the results of the Smiths’ approach using a sample permanent insurance policy, compared to a scenario in which they simply invested the tax refund in GICs. The potential insurance proceeds at each point in time result in a significantly greater estate value. It should be noted that the tax breaks inherent in a permanent life contract help to increase the eventual insurance proceeds and therefore the estate value.

Example 2

Joan Doe, 55, recently widowed, was left a substantial inheritance, and was meeting with her financial advisor to look at her own estate planning. After apportioning amounts to her nephews and nieces, given that she had no children of her own, Joan was seeking a way to leave money to support 3 of her favourite passions.

A lifelong patron of several cultural organizations, Joan decided she wanted to provide an endowment to the Symphony Orchestra, the Opera Company, and the Museum. With $1,000,000 left to divide amongst the 3, Joan was hoping her advisor could suggest something that could maximize the donations.

On his recommendation, Joan agreed to deposit the $1,000,000 over 8 years into a permanent insurance plan. With the growth in the policy, when Joan passes away, the policy will pay approximately $1,000,000 to each organization, effectively tripling Joan’s contribution. (Empire Life, Estatemax 8 Pay)

How Can You Calculate Your Tax Benefit Credit?

In Canada, various provinces and territories have slightly different rates for tax benefits as a result of charitable contributions, so it’s important to ensure you’re computing your tax credits with the correct rate for your area.

This content is provided for general informational purposes only and does not constitute financial, investment, tax, legal or accounting advice nor does it constitute an offer or solicitation to buy or sell any securities referred to. Individual circumstances and current events are critical to sound investment planning; anyone wishing to act on this content should consult with his or her financial partner or advisor.

Serotyl

You could definitely see your skills within the work you write. The world hopes for even more passionate writers like you who are not afraid to say how they believe. All the time go after your heart.

Williamwat

Hello There. I discovered your weblog using msn. That is a really neatly written article. I’ll make sure to bookmark it and return to learn extra of your helpful information. Thanks for the post. I’ll definitely return.